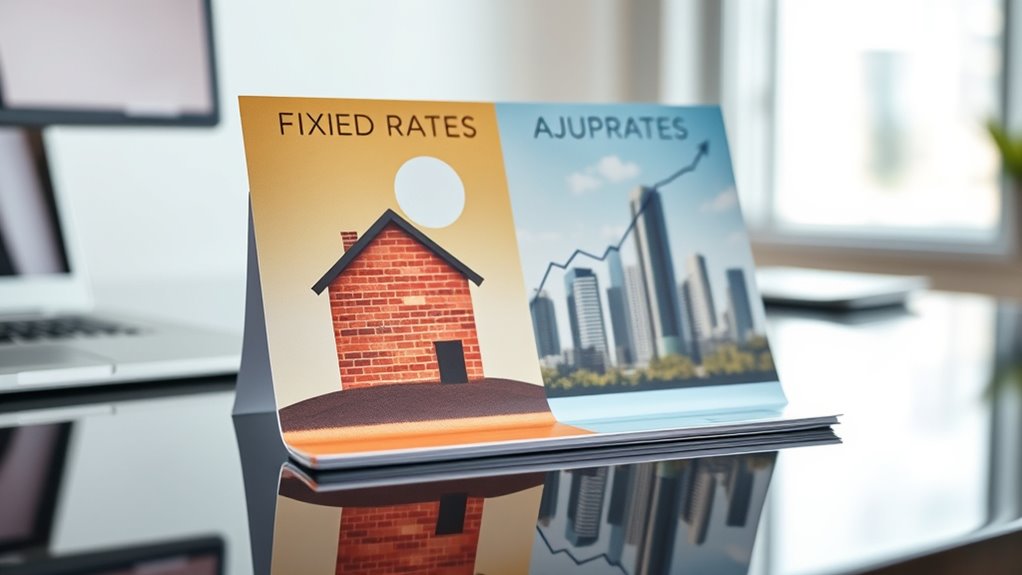

When choosing between fixed-rate and adjustable-rate mortgages, consider your financial stability and plans. Fixed rates stay the same, offering predictable payments, ideal for long-term stability. Adjustable rates start lower but fluctuate, which might save you money initially but can increase later. Think about your comfort with payment changes and future plans. To make the best choice, explore the critical differences and how they fit your goals. Keep going to uncover more helpful details.

Key Takeaways

- Fixed-rate mortgages have consistent interest rates, providing predictable monthly payments over the loan term.

- Adjustable-rate mortgages start with lower initial rates but fluctuate based on market conditions, affecting future payments.

- Fixed loans are ideal for long-term homeowners seeking stability; ARMs suit those planning to sell or refinance early.

- Qualification factors like credit score and income influence eligibility and the mortgage type you can secure.

- Refinancing options allow switching between fixed and adjustable rates to optimize payments and adapt to market changes.

Are you contemplating buying a home but feeling overwhelmed by the mortgage process? One of the first steps is understanding the different types of mortgage rates, especially fixed versus adjustable rates. When you’re exploring your options, you’ll need to consider how your loan qualification impacts your ability to secure a mortgage. Lenders look at your income, credit score, debt-to-income ratio, and savings to determine if you qualify for a loan. Once you’re qualified, you’ll want to weigh the stability of a fixed-rate mortgage against the potential savings of an adjustable-rate mortgage (ARM). Fixed-rate loans keep the same interest rate throughout the loan term, providing predictable monthly payments. This stability makes it easier to plan your finances long-term, especially if you prefer consistency or expect interest rates to rise in the future. On the other hand, adjustable-rate mortgages usually start with lower initial rates, which can be appealing if you’re comfortable with some uncertainty or plan to sell the home within a few years. With ARMs, your interest rate adjusts periodically based on market conditions, meaning your payments could go up or down over time.

Understanding refinancing options is also key when choosing between these two types. If you start with a fixed-rate mortgage, refinancing can help you take advantage of lower interest rates later or switch to an ARM if you want to reduce your monthly payments temporarily. Conversely, with an ARM, refinancing might be necessary if interest rates rise markedly, making your current loan more expensive. Keep in mind that refinancing involves applying for a new loan, which means you’ll need to go through the qualification process again, including credit checks and income verification. Depending on your financial situation, refinancing could lower your monthly payments or shorten your loan term, saving you money over the long run. Additionally, understanding risk assessment in mortgage options can help you better evaluate the potential for future payment fluctuations and financial stability.

Ultimately, your decision depends on your financial stability, future plans, and risk tolerance. If you prefer certainty and plan to stay in your home for many years, a fixed-rate mortgage offers peace of mind. If you’re comfortable with some fluctuation and want to capitalize on lower initial rates, an ARM might be suitable. Either way, understanding how loan qualification influences your options and knowing about refinancing can help you make confident choices. By weighing the benefits and risks of each rate type, you’ll better position yourself to choose the mortgage that aligns with your financial goals and lifestyle.

Calculated Industries 3400 Pocket Real Estate Master Financial Calculator

Loan Amortization and Remaining Balances

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

How Does a Hybrid Mortgage Work?

A hybrid mortgage combines features of both fixed and adjustable-rate loans. You start with a fixed interest rate for a set period, often 5 to 10 years, providing predictable payments. After that, the rate adjusts periodically based on market conditions. When qualifying for the loan, lenders consider your ability to handle potential interest rate changes. Interest calculations during the fixed phase are straightforward, but they switch to variable adjustments afterward.

Can I Switch Between Fixed and Adjustable Rates Later?

Yes, you can switch between fixed and adjustable rates later. You’ll explore refinancing options to make this change, so staying informed about interest rate trends helps you decide the best time. Imagine locking in a fixed rate during uncertain times or switching to an adjustable rate when rates drop. This flexibility allows you to adapt your mortgage to your financial goals, ensuring you’re always making the most of current market conditions.

What Are the Tax Implications of Each Mortgage Type?

You can deduct mortgage interest on your taxes, but the rules differ for fixed and adjustable-rate mortgages. With fixed rates, you’ll often benefit from consistent deductions, while adjustable rates may mean fluctuating interest deductions due to interest limitations. Keep in mind, the IRS caps mortgage interest deductions if your loan exceeds certain limits. Always consult a tax professional to understand how each mortgage type impacts your specific tax situation.

How Do Economic Changes Impact Adjustable-Rate Mortgages?

Imagine your adjustable-rate mortgage is on a roller coaster, wildly bouncing with every economic change! Interest rate fluctuations can send your payments soaring or plunging, making budgeting a nightmare. Economic policy impacts, like rate hikes or cuts, directly influence your mortgage costs, turning your financial stability into a game of chance. Staying alert to these shifts helps you prepare for the wild ride and avoid surprises that could upend your finances.

Are There Any Penalties for Refinancing Fixed or Adjustable-Rate Mortgages?

Yes, there can be penalties for refinancing your fixed or adjustable-rate mortgage. Prepayment penalties might apply if you refinance early, which can increase your refinancing costs. These penalties vary by lender and loan terms, so it is crucial to review your mortgage agreement. Keep in mind that some lenders waive prepayment penalties after a certain period, but always factor in refinancing costs when deciding whether to refinance.

Consumer Handbook on Adjustable-Rate Mortgages

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Conclusion

Choosing between fixed and adjustable-rate mortgages is like picking the right sailing course—you want a steady breeze or the flexibility to catch changing winds. Understand your financial goals and risk comfort, and you’ll steer confidently toward the best option. Remember, the right mortgage can be your sturdy ship through life’s waters, guiding you home. So, weigh your options carefully and set sail toward your dream house with confidence!

MORTGAGE REFINANCING OPTIONS AND BENEFITS OF REFINANCING MORTGAGE

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

HOME LOAN CLARITY: A First-Time Buyer's Guide to Smart Homeownership

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.